Emcure Pharmaceuticals Company is coming up with its IPO fresh issue of Rs. 800 crore and offer for sale worth Rs. 1,152.03 crore, which will open on 3rd July 2024. The issue will close on 5th July 2024 and be listed on the exchange on 10th July 2024. In this article, we will look at Emcure Pharmaceuticals IPO 2024 and analyze its strengths and weaknesses. Keep reading to understand about the company.

Emcure Pharmaceuticals IPO 2024 – About the Company

Emcure Pharmaceuticals was incorporated in 1981. Emure Pharmaceuticals manufactures, develops, and markets a wide range of pharmaceutical products across various therapeutic areas. They are also involved in research and development, with a product portfolio that includes orals, injectables, and biotherapeutics.

They are in over 70 countries worldwide, including strong markets such as India, Europe, and Canada.

In the domestic market, the majority of their revenue comes from a differentiated product portfolio that has increased presence in most of the major therapeutic areas, such as cardiovascular, gynecology, minerals and nutrients, vitamins, HIV antivirals, blood-related, and oncology/anti-neoplastics.

Note: If you want to learn Candlesticks and Chart Trading from Scratch, here’s the best book available on Amazon! Get the book now!

By September 2023, Emcure Pharmaceuticals had 28 brands available for domestic sales, up from 13 in September 2019. They also sell their portfolio of differentiated products in more than 70 countries. Emcure owns front-end distribution or focuses on alliances with other companies to increase their international presence.

Emcure operates 13 manufacturing facilities in Sikkim, Gujarat, Maharashtra, Karnataka, and the union territory of Jammu and Kashmir. Their R&D team consists of 552 qualified scientists and around 5,000 field agents who interact with healthcare providers.

Emcure Pharmaceuticals IPO 2024 – About the Industry

India’s level of pharmaceutical usage reflects both a very minimal healthcare infrastructure and ease of access to medicines, with even the most sophisticated medicines being widely available. The average pharmaceutical usage gap between developed and emerging markets is decreasing as per capita income rises and healthcare infrastructure improves.

In recent years, the Indian domestic formulation market has expanded steadily. As of the Financial Year 2023, the Indian domestic formulation market accounted for roughly 2-3% of the overall global pharmaceutical market. Indian domestic formulations market. The domestic formulations market expected to increase at a 9-10% CAGR from Fiscal Year 2023 to Fiscal Year 2028.

The chronic therapies segment of the Indian domestic formulation market is expected to grow at a CAGR of 10-11% between Financial Year 2023 and Financial Year 2028, while the acute therapies segment is expected to grow at a CAGR of 9-10% between Financial Years 2023 and 2028.

As India is one of the world’s leading manufacturers of pharmaceutical products, global MNCs are expected to capitalize on this advantage and attempt to collaborate with Indian players for drug manufacturing or co-marketing to establish a strong presence in the growing Indian pharmaceutical market.

Emcure Pharmaceuticals IPO 2024 – Financial Highlights

Emcure reported revenue from operations of Rs. 5,985.81 crore in FY23, up 2.22% from Rs. 5,855.38 crore in FY22. Net profits in FY23 were Rs. 561.84 crore, a decrease of 20.02% from Rs. 702.55 crore in FY22. The finance cost increase has impacted its profitability, which has been growing since FY21.

Emcure Pharmaceuticals’s current borrowings contribute around 2/3rd of the total borrowings. It projects the need for working capital for operations as pharma is a capital-intensive business.

The RoE in FY23 stood at 21.27%, down from 33.32% in FY22. RoCE is more relevant as the interest cost is high and in FY23, the ratio stood at 22.01% compared to 29.69% in FY22.

Emcure generates most of its revenue from the sale of products, which accounts for 98.13%, with the remaining 1.87% coming from services and other operating revenues in FY23. They recognised their revenue segment under pharmaceuticals.

Emcure Pharmaceuticals’s revenue exposure across geographies was 53.15% from India, (down 0.71% YoY), 19.83% from Europe (up 32.46% YoY), 12.18% from North America (up 7.35% YoY), and the remaining 14.82% from other continents, (up 17.42% YoY) in FY23.

Emcure Pharmaceuticals IPO 2024 – Key Players

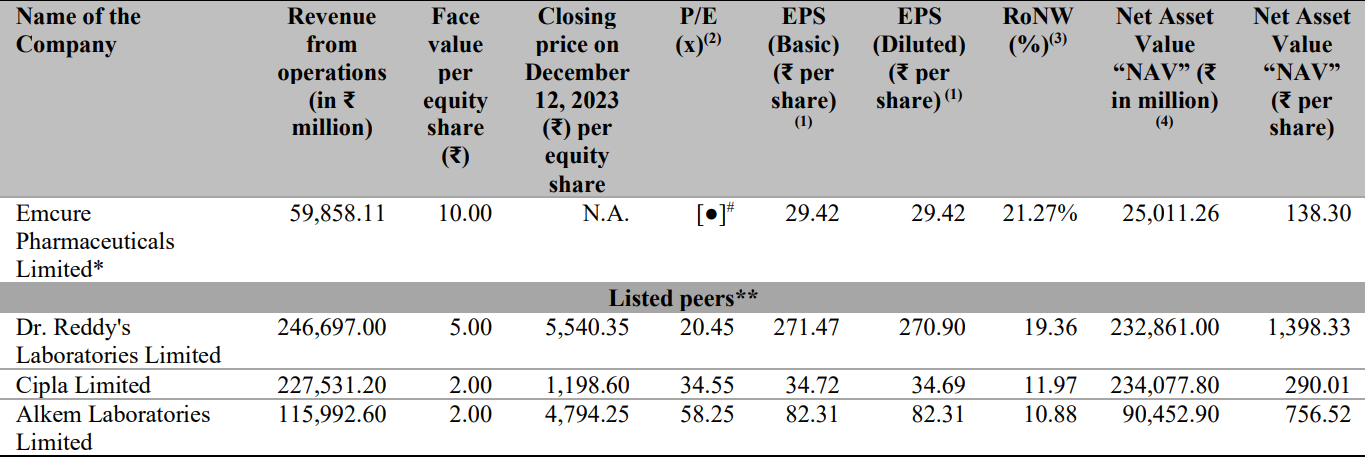

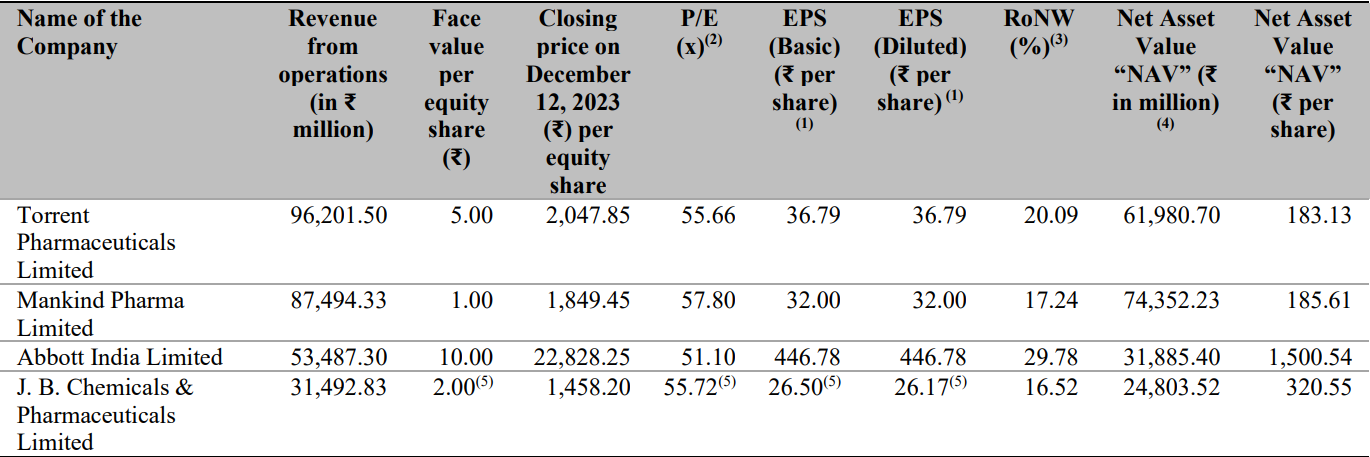

Emcure Pharmaceutical’s listed peers are Dr. Reddy’s Laboratories Limited, Cipla Limited, Alkem Laboratories Limited, Torrent Pharmaceuticals Limited, Mankind Pharma, Abbott India Limited, and J.B. Chemicals & Pharmaceuticals Limited.

Compared to its peers, revenue exposure for Emcure in India is around 53% in FY23, whereas Mankind, Abbott India, and Alkem Laboratories are higher than Emcure.

The EBITDA margins of Emcure are around 20% in FY23, compared to its peer’s margins of around 22-30%. Emcure has underperformed its peers in EBITDA margins.

Emcure’s return on equity is around 21.27%, which is better compared to its peers. Abbott India has a better ROE, but Emcure had more than 20% in FY23, which is marginally higher than its peers.

Source: RHP of the company

Strengths of the Company

- Diversified Manufacturing Capacity: Emcure Pharmaceuticals has around 13 manufacturing facilities across India. They began as a contract development and manufacturing organisation for other corporations. This helped the company handle complex manufacturing processes. The ability has also assisted them in producing their Active Pharmaceutical Ingredient (API), allowing them to source products more cost-effectively.

- Diverse product portfolio for International markets: Emcure has a presence in over 70 countries, and by adding new products, the company can deepen its presence while also factoring in regulatory constraints, which can help it gain more market share and grow its revenues.

- Product Brand Building: The company was able to demonstrate its ability to monetise its products as its 8 brands were ranked among the top 300 highest-selling brands in Indian Pharma Market. Based on the most recent moving annual total for September 2023, their top-selling therapeutic areas were gynecology, vitamins, minerals, and nutrients, anti-infectives, respiratory, and so on.

- Well-positioned in the Domestic Market: The company’s revenue from operations, half of the exposure is from India. Emcure is the 13th largest pharmaceutical company in India based on MAT September 2023. Their products are differentiated and specialist prescription-based contributing around 70% of total prescriptions for MAT (Moving Annual Total) October 2023. This is similar to a well-known product on the market, giving it an advantage over competing products.

- Experienced Management: Emcure Pharmaceuticals management is experienced and capable. The promoters have diverse backgrounds and have various fields of expertise. It is a family-run business. Their chief scientific officer has significant experience in pharmaceutical sciences and has been involved in various advanced research projects. The ability to manage and overcome situations shows the agility of the management.

Weaknesses of the Company

- Working capital requirements: The company’s majority of its total borrowings are current borrowings. Cash flow can be impacted due to the cost of operations, procurement of raw materials, development of products, and the delay in payment received from customers. The pharma industry is highly capital intensive and R&D expenditure requires consistent capital to bring new products.

- Pricing Pressure on Products: The impact on product pricing can be under pressure due to the dynamics of the market, as nearly half of the company’s revenue comes from overseas. Competition from other pharma companies can affect profitability margins.

- Commercialising R&D efforts: The introduction of new products is crucial to expanding its market share and is in line with regulatory standards. The company might be adversely impacted if they do not succeed in monetising its R&D efforts. The uncertain outcomes can hinder the time and expenses associated with risk.

- Government Regulations: Emcure operates in a highly regulated industry and its operations, manufacturing, and quality maintenance are crucial to keeping the products within regulatory limits. FDA or any local governing body that issues any restrictions can have an impact on its operations.

- Distribution and Marketing: Being present in multiple markets carries significant risks, as increased competition can reduce product sales. There might be an increased risk of selling products through third-party entities on other continents, as the company does not hold any control over the distribution or the dynamics of the market.

Also read…

Emcure Pharmaceuticals IPO 2024 – GMP

The shares of Emcure Pharmaceuticals is traded at a premium of 26% in the grey market as of July 1st, 2024. It traded at Rs 1,272 which gives it a premium of Rs 264 over its higher cap of Rs 1,008 per share.

Emcure Pharmaceuticals IPO 2024 – Key IPO Information

Promoters: Satish Ramanlal Mehta and Sunil Rajanikant Mehta

Book Running Lead Manager: Kotak Mahindra Capital Company Limited, Axis Capital Limited, Jefferies India Private Limited and J.P. Morgan India Private Limited.

Registrar to the Offer: Link Intime India Pvt Ltd.

The Objective of the Issue

- To reduce outstanding borrowings taken by the company.

- General corporate purposes.

Conclusion

Emcure Pharmaceuticals, with its diverse portfolio and international presence, has the potential to increase revenues and improve profitability. The high capital-intensive nature of the pharmaceutical industry limits its ability to generate additional profits. The higher the volume growth, the better for the company. The quality of manufacturing is of utmost importance, as any issues can attract regulatory action and its prospects are aligned with the demand and based on new products from the company.

So what do you make of this company? Will it be able to maintain its margins based on its competition with peers? What is your view? Let us know in the comments below.

Written by Santhosh

By utilizing the stock screener, stock heatmap, portfolio backtesting, and stock compare tool on the Trade Brains portal, investors gain access to comprehensive tools that enable them to identify the best stocks, also get updated with stock market news, and make well-informed investments.

Start Your Stock Market Journey Today!

Want to learn Stock Market trading and Investing? Make sure to check out exclusive Stock Market courses by FinGrad, the learning initiative by Trade Brains. You can enroll in FREE courses and webinars available on FinGrad today and get ahead in your trading career. Join now!!