FirstCry Company is coming up with its IPO of Rs 4,193.73 Cr of which Rs. 1,666 crores is fresh issue and the remaining will be offer for sale worth Rs. 2,527.73 crores. The IPO open on 6th August 2024. The issue will close on 8th August 2024 and be listed on the exchange on 13th August 2024. In this article, we will look at FirstCry IPO Review 2024 and analyze its strengths and weaknesses. Keep reading to learn about the company.

FirstCry IPO Review – About the Company

FirstCry was incorporated in 2010. By the use of FirstCry as a platform they are one of India’s biggest multi-channel retail platforms for mothers, babies, and kids products. The company with domestic presence and looking for an international presence.

They’ve even expanded to the UAE and Saudi Arabia. FirstCry sells products online through its app and website, in its stores, and through franchisee-owned shops. They also distribute products to other retailers. FirstCry offers over 1.65 million items from 7,580 brands, including their home brands like BabyHug.

For brand building, they’ve got a parenting community with helpful content and tools. FirstCry has also branched out into education, running preschools and selling educational toys.

Note: If you want to learn Candlesticks and Chart Trading from Scratch, here’s the best book available on Amazon! Get the book now!

The diversification strategy helps FirstCry to tap into new markets and revenue streams and hold on to its core business of families and kids.

FirstCry IPO Review – About the Industry

India’s retail industry is on an increasing trend, with e-commerce leading the way. More people are getting online access, mainly from smartphones and better internet connections. By 2029, there might be a billion internet users and up to 350 million online shoppers. The increase in potential customers through the Internet provides an opportunity.

The e-commerce market is set to grow about 20% each year expecting to touch around $157 billion by 2029. People in smaller cities like tier 2 and 3 are getting access to the internet and an increase in awareness. This helps companies to leverage these aspects and can tap into these markets.

With the upward trend of the population in India, parents are spending more on their kids. They’re buying more childcare products as they become more aware of child health and have more money to spend. This market is growing faster than in the US or China.

FirstCry IPO Review – Financial Highlights

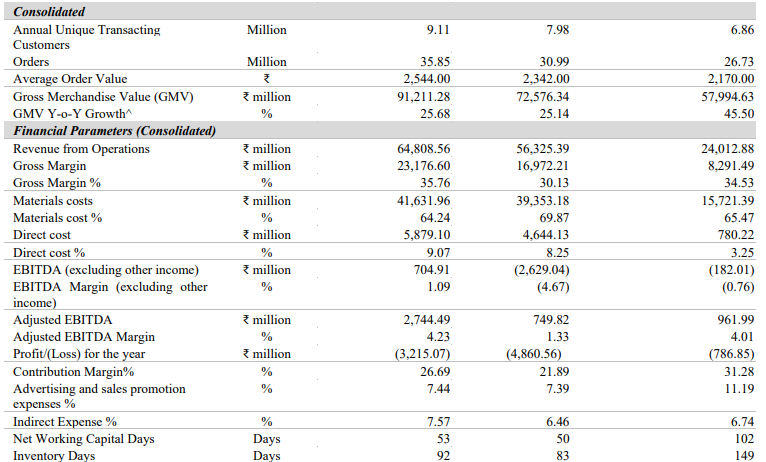

FirstCry (Brainbees Solutions) reported revenue from operations of Rs. 6,480.85 crores in FY24, up 15.06% from Rs. 5,632.53 crores in FY23. Losses in FY24 were Rs. 321.50 crore, an increase of 33.85% from Rs. 486.05 crore in FY23. There was an improvement in Material Costs, Employee benefits expenses, purchase of stock, finance costs, and other expenses which have limited its losses.

The earnings per share in FY24 was Rs. -6.20 per share which was an improvement of 37.81% from the previous year’s Rs. -9.97 per share. There was an improvement in EPS, based on the cost control with increasing revenue.

Retail business is capital intensive and Brainbee’s equity value is positive, the company’s gearing ratio in FY24 stood at -0.07 compared to -0.29 in FY23. The negative gearing ratio exists because the company has excess cash after the debt is repaid. It is good if the ratio is below, but the trend has decreased YoY in this case.

FirstCry recognises its revenue from operations under India multi-channel, GlobalBees Brands, International, and Others. In India multi channel it contributes 70.66% of the revenue, International – 11.63%, Globalbees brand – 18.66%, and others – 0.51% in FY24.

FirstCry IPO Review – KPI Highlights

The consolidated Gross Merchandise Value (GMV) stood at Rs. 9,121.12 crore compared to Rs. 7,257.63 crore in FY23. Their average order value in FY24 stood at Rs. 2,544 against Rs. 2,342 in FY23 which is a decent growth. Their order volume grew to 3.58 crore in FY24 improved from 3.09 crore in FY23.

The advertisement cost in FY24 is Rs. 482.18 crore, which is around 7.44% of its operating revenues, and Rs. 416.47 crore in FY23. Courier charges were Rs. 545.74 crore in FY24, up 27.13% from Rs. 429.27 crore, contributing 8.42% of the revenue in FY24. These expenses take the majority of the profits.

FirstCry IPO Review – Key Players

The company mentioned that similar to their business or even to a comparable size, there are no listed Companies in their RHP.

Strengths of the Company

- Tapping Kids Retail Market: The company operates India’s largest multi-channel retailing platform for mothers, babies, and kids products. Its GMV increased to ₹91,211.28 million in FY2024 from ₹57,994.63 million in FY2022, showcasing its growth and market leadership.

- Marketing Campaigns: The company’s content-led strategy drives network connections. Its FirstCry.com parenting platform features expert content, attracting customers organically. The mobile app had over 127 million downloads by March 2024, which has increased engagement and transactions.

- Customer Retention: The company has built a strong brand and customer loyalty. Its Annual Unique Transacting Customers grew to 9.11 million in FY2024. Existing customers generated 72.23% of GMV in FY24.

- Diverse Products: The company offers a diverse product range through third-party and home brands. They added 1,125 new brands in FY24 and had 7,580 associated brands.

- Leveraging Data for Business Penetration: The company leverages technology and data for personalized customer experiences. They use geolocation tags, cross-channel sales data, and customer profiles to offer tailored product suggestions and content.

Weaknesses of the Company

- Rental Market Risks: The company relies on leased properties for its modern stores. This exposes it to rental market fluctuations and risks associated with lease renewals, potentially leading to store closures or relocations that could affect overall sales and incur additional costs.

- Manufacturing Dependence: The company lacks exclusive agreements with contract manufacturers, suppliers, and third-party brands. This allows these manufacturers to work with competitors as well.

- Change in Customer Behaviour: The company’s business depends significantly on the growth of online commerce in India. If the industry fails or if the company is late in adopting changing customer behaviors on digital platforms, that can have adverse effects on its operations.

- Financial Risk of its Subsidiaries: Several subsidiaries face financial challenges, with auditors noting material uncertainties about their ability to continue as going concerns. The parent company provides financial security for these subsidiaries, which could strain resources.

- Highly Competitive Market: The company operates in a highly competitive industry, facing rivals like Reliance Retail, Gini & Jony, Amazon, Flipkart, and Meesho. The company holds only a 2.5-3% market share in the India Childcare products market. Intense competition could hinder growth strategies and impact profitability.

Also read…

FirstCry IPO Review – GMP

The shares of FirstCry’s price in the grey market were trading at an 18.49% premium as of August 1st, 2024. The shares in Grey Market traded at Rs.551. This gives it a premium of Rs.86 per share over the cap price of Rs. 465.

FirstCry IPO Review – Key IPO Information

Promoters: No Identifiable Promoter.

Book Running Lead Manager: Kotak Mahindra Capital Company Limited, BofA Securities India Limited, Morgan Stanley India Company Private Limited, JM Financial Limited and Avendus Capital Private Limited.

Registrar to the Offer: Link Intime India Private Limited.

The Objective of the Issue

- Expenditure for the company to set up new stores under the “BabyHug” brand and set up a warehouse in India.

- Lease payment expenses for the existing stores owned and controlled by the company.

- Investing into Digital Age, a company’s subsidiary to set up new stores under the FirstCry brand and other home brands, lease payments for stores controlled and owned by Digital Age in India.

- Investment in the subsidiary, FirstCry Trading for setting up stores and warehouses for overseas expansion in the Kingdom of Saudi Arabia.

- Investment in the company’s subsidiary, Globalbees Brands to acquire additional stake in step-down subsidiaries.

- Sales and marketing initiatives.

- Technology and data science costs which include cloud and server hosting costs.

- Funding inorganic growth through acquisitions & other initiatives.

- General Corporate Purposes.

Conclusion

FirstCry has a good presence to grow from leveraging their platform “FirstCry”. However, the costs need to be controlled to reduce cash burn, thus focusing on profitability. The competition in this segment is still high considering many established players entering into this space. The brand value and product quality with better outreach can help increase their market share as well.

So what do you make of this company? Will it be able to increase its market share based on its competition with peers? What is your view? Let us know in the comments below.

Written by Santhosh

By utilizing the stock screener, stock heatmap, portfolio backtesting, and stock compare tool on the Trade Brains portal, investors gain access to comprehensive tools that enable them to identify the best stocks, also get updated with stock market news, and make well-informed investments.

Start Your Stock Market Journey Today!

Want to learn Stock Market trading and Investing? Make sure to check out exclusive Stock Market courses by FinGrad, the learning initiative by Trade Brains. You can enroll in FREE courses and webinars available on FinGrad today and get ahead in your trading career. Join now!!