CreditAccess Grameen: India’s microfinance industry is booming, fueled by rural credit demand and supportive policies. Despite this growth, domestic lending to the private sector remains low at 55% of GDP, lagging behind Asian peers. The sector’s potential is vast, with only 14% of MSMEs accessing formal finance. In this landscape, Credit Access Grameen emerges as a promising stock, leveraging its strong loan portfolio and focus on women entrepreneurs to capitalize on the expanding financial inclusion market.

Industry Overview

Microfinance refers to financial services provided to individuals or small enterprises that do not have access to traditional banking and related services. The economy currently has a shortfall of US 530 billion dollars. The credit gap exists primarily because it is difficult to handle the sector with minor funding requirements.

As a result, conventional lenders have avoided this space. However, with the recent advent of small-ticket MSME NBFCs, the credit gap has dramatically closed. Small loans are predicted to rise at a stunning rate of 23%, reaching $38 billion in 2024 from $25 billion in 2022. According to a survey, 80% of India’s microcredit portfolio is concentrated in 34% of districts. Therefore there is still an untapped share of 64% for the industry players.

Features of Microfinance

Some of the basic elements of microfinance include modest loan ticket sizes, and lack of collateral requirements, and borrowers are primarily from the poorer sections of the society and do not have access to regular borrowing facilities as conventional loan sources require a mortgage.

Note: If you want to learn Candlesticks and Chart Trading from Scratch, here’s the best book available on Amazon! Get the book now!

Company Overview Of CreditAccess Grameen

CreditAccess Grameen Limited is an Indian Microfinance institution that was incorporated in the year 1999 by Vinatha M. Reddy. Headquartered in Bangalore, it boasts of having operations in 16 states and 1 union territory. The company was listed on NSE and BSE in August 2018, in a ₹ 1,131Cr. IPO.

Deals: In September 2019, Citigroup collaborated with CA Grameen to fund 75,000 women entrepreneurs in India. CreditAccess also bought Madura Micro Finance in November 2019 for Rs. 876 crore. In 2022, the company signed a contract of $35 million with the US International Development Finance Corporation. CA Grameen has also inked a syndicated social credit facility worth $200 million, making it a pioneer in the microfinance market and the fourth in the country.

Financial Highlights Of CreditAccess Grameen

The company’s net interest income has increased by more than 3 fold from 1,092.3 Cr. in 2020 to 3,259.6 Cr. In 2024. The company’s net profit and earning per share have increased by 4 times from ₹ 328Cr.(2020) to 1,446 Cr.(2024) and ₹22.75 (2020) to ₹90.72 (2024) respectively. Additionally, Credit Access was also greatly successful in bringing down its GNPA which had gone past 4% in 2021 to 1.18% by creating provisions.

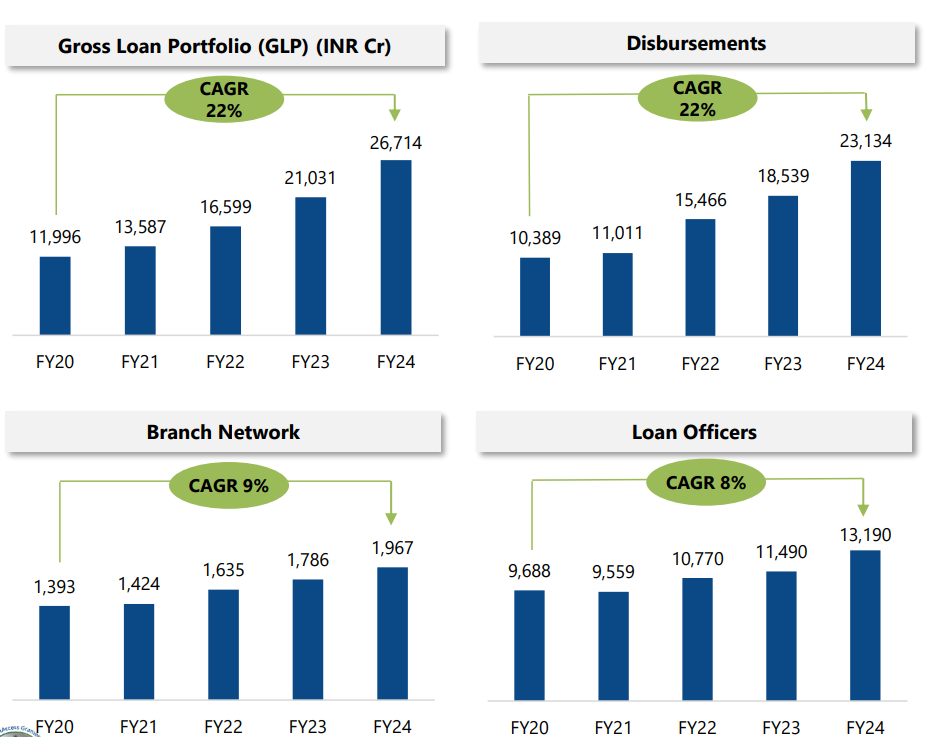

Key Performance Indicators

Over the last 5 years, Gross Loan Portfolio and Disbursements have gone up by 22% CAGR from 11,996Cr. to 26,714Cr. and 10,389Cr. to 11,011Cr. respectively. Aside from that, there has also been a healthy expansion in terms of branch network and loan officers, both growing at a pace of 9% and CAGR 8% respectively.

Competitors

Some of the biggest competition to CreditAccess comes from established players and market leaders of the industry like Bajaj Finance, Mahindra & Mahindra Financial Services Ltd. and similar size companies like Spandana Sphoorty Finance Ltd. and Satin Creditcare Network Ltd. All these companies are trying to reach out to the same target addressable market.

Satin Creditcare Network Ltd: is a leading microfinance company with a presence over 23 states and Union Territories and has operations in over 95,000 villages across the country. It provides a range of services from microfinance loans to business correspondent services.

Spandana Sphoorty Financial Ltd: they are registered with RBI as NBFC-MFI. The company is primarily engaged in the business of microfinance providing small-value unsecured loans to low-income customers in semi-urban and rural areas.

Mahindra & Mahindra Financial Services Ltd: is an NBFC and a part of the Mahindra group. The company is primarily engaged in the business of financing the purchase of vehicles, construction equipment, and SME financing.

Key Metric of Competitors

Asset Quality

CreditAccess Grameen has demonstrated overall improvement in asset quality. As of Q4 FY24, Gross Non-Performing Assets (GNPA) stood at 1.18%, down from 1.21% in Q4 FY23. Net NPA improved to 0.35%, while Portfolio at Risk (PAR) 90+ days decreased to 0.94% from 0.96% a year ago. To cover for the expected credit loss, provision was increased to 1.95%, reflecting conservative practices.

Collection efficiency (excluding arrears) remained robust at 98.3%. Write-offs for FY24 totaled INR 296.2 crore, or 1.5% of the March 2023 on-book loan portfolio. However, the company’s PAR 0+ showed a slight increase, rising from 1.5% in Q4 FY23 to 1.7% in Q4 FY24. Despite this small uptick, the overall trends highlight CreditAccess Grameen’s effective risk management and its ability to maintain strong asset quality in the microfinance sector.

Also read…

Future Outlook Of CreditAccess Grameen

CreditAccess Grameen plans to achieve 12-15% NIM of total AUM by FY27-28. Furthermore, they intend to address the issue of client attrition by introducing new products and services. Additionally, the corporation plans to increase its market share by expanding into new geographical areas. CreditAccess is likewise seeking to diversify its risk profile. Lastly, the corporation hopes to maintain a leverage of at least 20% of its capital.

Price Targets

Geojit BNP Paribas: has given a “BUY” rating on the stock, with an upside potential of 15% up to the levels of ₹ 1,628 owing to its improving EPS and strong FInancing Margin.

KR Choksey: has given a “BUY” rating on the stock with a price target of 1800+ as CreditAccess’ NII came at 33.6% YoY and beat the NII estimate by 4.7%.

Axis Securities: continues to maintain its stance of “BUY” recommendation with an upside potential of 35% to the level of 1900+ because of its improving fundamentals.

Conclusion

In conclusion, it will be interesting to see how the stock moves in the forthcoming days. Will it be able to broaden its horizons and capitalize on the credit gap that exists in the Indian economy? Will it be able to maintain its top position against the new entrants in the segment? Comment your thoughts below.

Written By Dipangshu Kundu

By utilizing the stock screener, stock heatmap, portfolio backtesting, and stock compare tool on the Trade Brains portal, investors gain access to comprehensive tools that enable them to identify the best stocks, also get updated with stock market news, and make well-informed investments.

Start Your Stock Market Journey Today!

Want to learn Stock Market trading and Investing? Make sure to check out exclusive Stock Market courses by FinGrad, the learning initiative by Trade Brains. You can enroll in FREE courses and webinars available on FinGrad today and get ahead in your trading career. Join now!!